How do the wealthy get away with paying a lower percentage of their income and wealth in taxes than ordinary people? A big part of the answer is that many of their fortune streams – from dividends to inheritance – are chronically undertaxed, says Chiara Putaturo in our latest blog for Davos 2023

Oxfam’s report for this week’s Davos gathering traces the remarkable decline in taxes on the rich – and the explosion in wealth of the top 1 percent that has followed. In this blog, I want to unpack why the top 1 percent often get away with much lower taxes in proportion to their income and wealth than the rest of us.

The crucial point is that this is not just about falling tax rates over the past decades: in fact, the rich also tend to pay less because the forms of income they often rely on are taxed much lower than the income of a typical person who has to rely on a salary.

‘Half of the world’s billionaires are from countries with no inheritance tax… these super-wealthy people will be able to pass on a combined fortune of $5 trillion completely tax-free to the next generation’

Here are seven typical forms of income and wealth for the richest that are often undertaxed:

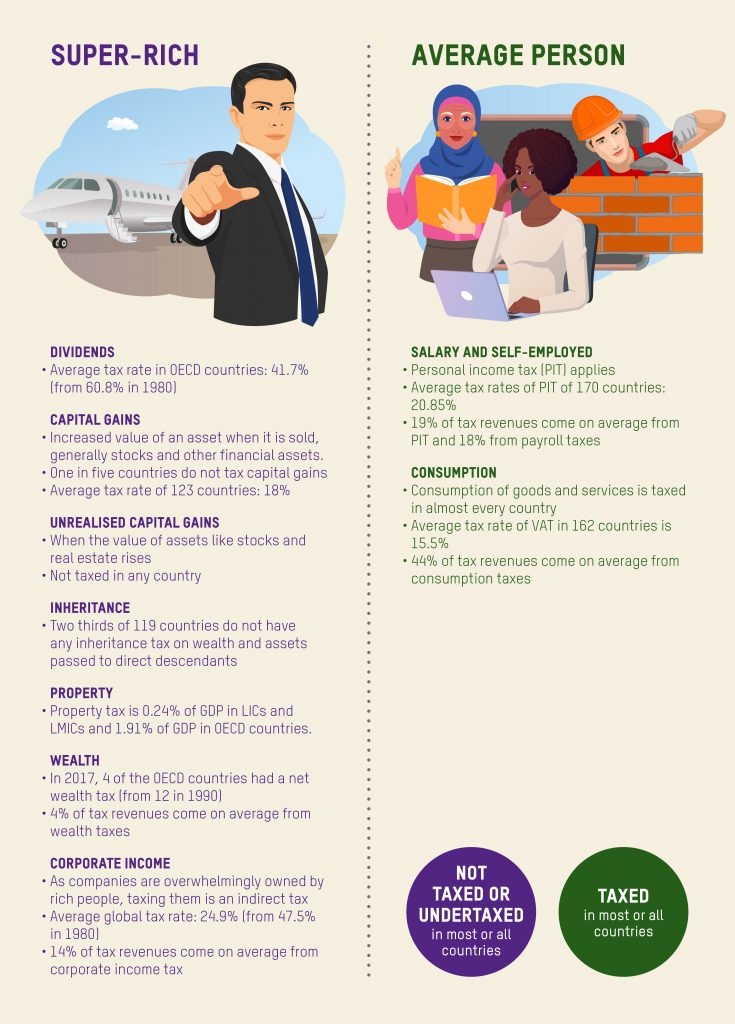

1. Dividends, that is the money that shareholders of a company receive regularly out of the profits of the company. The tax rate on dividend in the OECD countries dropped from 60.8 in 1980 to 41.7 recently. (You can find the methods we used to obtain this and other numbers here.)

2. Capital gains, that is the increase in value of an asset when it is sold. Capital gains are more unequally distributed than income and wealth. This is even true in one of the most equal countries in the world, Denmark, where the richest 1 percent receive more than half of all capital gains. Oxfam’s analysis of 123 countries shows that one in five countries do not tax capital gains, and that the average tax rate on capital gains is only 18%. Our research found only three countries that tax capital income more than work income.

3. Unrealised capital gain, that is the increase in value of an asset before it is sold. Unrealised capital gains are generally not taxed and this allows rich people to accrue value from their assets without having to pay tax on it. Moreover, assets (financial, property, etc.) can be used as collateral to raise loans. Therefore, even if they are “unrealised”, these gains can in practice be turned into real money for the wealthiest and contribute to growing their fortunes further.

4. Property, including land and buildings. Property ownership generally remains concentrated in the hands of the wealthy. The revenue-raising potential of property taxation is particularly significant in low- and lower-middle-income countries, where it is 0.24% of GDP (compared with 1.91% of GDP in OECD countries). If all low- and lower-middle-income countries raised as much revenue from property taxation as Morocco, where it is equivalent to 1.26% of GDP, they could collect an additional $17.6bn.

5. Inheritance, that is the value of all possessions transferred to some someone else upon an individual’s death. Of the 119 countries Oxfam reviewed, only 33% tax inheritance passed to direct descendants and for low- and lower-middle-income countries the figure is even lower. That means half of the world’s billionaires (46%) are from countries with no inheritance tax on wealth and assets passed to direct descendants. These super-wealthy people (1,232 people) will be able to pass on a combined fortune of $5 trillion completely tax-free to the next generation, keeping the concentration of wealth in the hands of the same families, and perpetuating inequality. That is more than the entire GDP of Africa.

6. Wealth: the value of all assets of an individual within the country or offshore: housing, bank deposits, corporate stocks, financial assets or tangible assets (e.g. jewellery, paintings, yachts). The world’s wealth is concentrated in the hands of the few and is severely under-taxed almost everywhere.

Across 88 countries Oxfam estimates that only 4 cents in every dollar raised in tax revenue comes from taxes on wealth, such as property taxation. In 1990 there were 12 OECD countries with a net wealth tax. Since then, net wealth taxes have been abolished in one country after another and in 2017 only 4 of the OECD countries still had a net wealth tax.

The IMF has underlined the important role that wealth taxes could play in reducing inequality. It recently estimated that across 21 rich countries and three ‘emerging’ economies, an annual net wealth tax of just 1% could reduce the wealth share of the richest 1% by between one and 2.5 percentage points over a 20-year period, and that this could reduce the wealth concentrated in their hands by more than 10%.

7. Corporate income. Tax levied on corporate profits. Even if it is not levied directly on the rich, there is increasing evidence that wealthy shareholders pay the majority of this tax. Corporate income tax has globally fallen from an average of 47.5% in 1980 to 24.9% today. This is especially important right now, as several companies are posting record profits.

Our analysis shows that 95 companies in the food and energy sector made windfall profits of $306bn in 2022, growing more than 256% compared to their average for 2018-2021. 84% of their windfall profits – $257bn – was paid out as dividends to their shareholders, illustrating how high corporate profits translates into money in the hands of the rich (who are heavily overrepresented among shareholders) when they are not taxed sufficiently.

How ordinary people shoulder the tax burden

An average person does not benefit, or only benefits to a limited extent, from these forms of income and wealth. The majority of taxes that an ordinary citizen pays are on the income from work (both salaried and self-employed) and goods and services. Rich people also pay Personal Income Tax (PIT) on their work income and on consumption, but both of these add up to a smaller proportion of their income because of all their other income streams. (Oxfam calculated that the average rate of PIT and VAT – value-added tax on things people buy – is 20.85% and 15.5% respectively.)

‘Despite the fact that VAT is generally regressive, the number of countries applying this tax tripled between 1990 to 2017, from 50 to more than 150’

Today, taxes falling on citizens, be it through personal income, payroll (taxes for social security and health funds) or consumption, account for more than 80% of total tax revenue (19% from PIT, 18% from payroll taxes and 44% from consumption taxes). Moreover, VAT tends to fall disproportionally on the poorest people, because they spend higher share of their income on consumption. Despite the fact that VAT is genrally regressive, the number of countries applying this tax tripled between 1990 to 2017, from 50 to more than 150.

Meanwhile, Personal Income Tax has become less progressive, with marginal rates on the top earners declining from 58% in 1980 to 42% today in OECD countries, and similar trends for countries in Africa, Asia and Latin America. Oxfam estimates that across 100 countries the average top personal income tax rate now stands at only 31%.

All of that is why rich people often end up paying less tax in proportion to their income and wealth than an average person. This contributes to inequality, harms the social contract, and means that billions that could be invested in inequality-busting sectors – healthcare, education, food security, and in the just transition to clean energy – goes uncollected. This has to change, and change now.

Author

Want to find out more? Read Oxfam’s report for the Davos meeting, “Survival of the Richest: How we must tax the super-rich now to fight inequality”. You can find a full account of how we worked out key numbers used in this blog and the report in this methodology note.

This is the third in a series of blogs for Davos. Follow us on Twitter and LinkedIn to keep up with the latest Davos content and subscribe to our monthly round-up of Oxfam blogs and research.

The blogs are also posted on Oxfam’s brilliant Equals site, where you can find blogs and podcasts about global inequality – and they’ve just launched an Equals Substack newsletter. Read the first newsletter, all about Davos, and subscribe now.